benzinga.com

benzinga.com fool.com

fool.com

For most retirees, Social Security represents an indispensable financial lifeline.

Since 2002, national pollster Gallup has been surveying retirees annually to gain perspective on how reliant they are on the income they receive from America’s top retirement program. These surveys show that 80% to 90% of respondents, including 88% in 2024, require their Social Security check to cover at least some form of their monthly expenses.

Considering how important Social Security income is to the financial well-being of seniors, former president and current Republican Party presidential nominee Donald Trump has proposed a plan to allow beneficiaries to hang onto more of what they receive. But as the former president is likely to discover, eliminating Social Security’s most-hated tax isn’t the cut-and-dried solution it appears to be.

Former President Donald Trump addressing reporters. Image source: Official White House Photo by Shealah Craighead.

Yes, Social Security benefits may be taxable

To be fair, there aren’t too many people who enjoy paying tax to the federal government. But among the varying taxes Americans are required to open their pocketbooks for, none are, arguably, as disliked as the taxation of Social Security benefits.

In 1983, Social Security’s asset reserves — i.e., the program’s excess cash built up since inception that’s invested in interest-bearing special-issue bonds, as required by law — were effectively running on fumes. Without action taken by Congress, Social Security’s payout schedule, including annual cost-of-living adjustments (COLAs), wasn’t expected to be sustainable. This paved the way for the Social Security Amendments of 1983.

The Amendments of 1983 represent the last major bipartisan overhaul for Social Security. It led to a gradual increase in payroll taxation and the full retirement age, as well as introduced the taxation of Social Security benefits.

Beginning in 1984, up to half of Social Security benefits could be exposed to federal taxation if provisional income — gross income, plus tax-free interest, plus one-half of Security benefits — topped $25,000 for single filers and $32,000 for couples filing jointly.

In 1993, the Clinton administration added a second tier to the taxation of benefits that allowed up to 85% of Social Security income to become taxable at the federal rate if the provisional income for a single filer or a couple filing jointly tops $34,000 or $44,000, respectively.

On top of Social Security benefits potentially being taxable at the federal level, nine states also tax Social Security income to some varying degree.

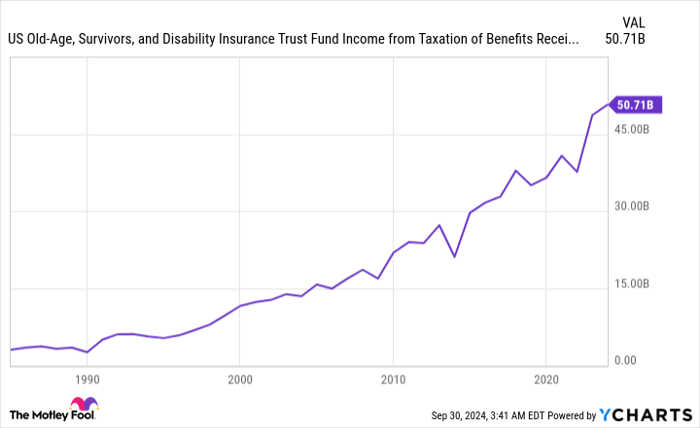

The taxation of benefits has grown into a more important source of income for Social Security over time. US Old-Age, Survivors, and Disability Insurance Trust Fund Income from Taxation of Benefits Receipts data by YCharts.

Donald Trump wants to end the federal taxation of Social Security benefits

The biggest issue with Social Security benefits being taxable isn’t the common misconception that this represents the double taxation of income. Rather, it’s that these two tiers of tax thresholds instituted by the Reagan and Clinton administrations have never been adjusted for inflation.

With the exception of 2010, 2011, and 2016, Social Security’s COLAs have been positive every year since 1975. This is to say that Social Security checks have increased on a year-over-year basis in 47 of the last 50 years. But because the provisional income thresholds haven’t increased with inflation since they were respectively introduced decades ago, more Social Security beneficiaries are being subjected to this tax over time.

According to an informal poll from nonpartisan senior advocacy group The Senior Citizens League, retirees really hate this tax. When asked, “Do you think Social Security should be included as taxable income for federal taxes?” a whopping 94% of the more than 5,300 respondents chose, “No.”

During a campaign rally in August, former President Trump stated to the crowd that, “Seniors should not pay taxes on Social Security and they won’t.”

Among the various proposals Trump and his campaign have put forth, such as a 60% tariff on goods imported from China, a potential lower corporate tax rate, and a flurry of proposed personal income tax breaks, nothing is likely to be more popular than putting an end to the taxation of Social Security benefits.

However, simply halting the taxation of Social Security benefits for select recipients could ultimately do more harm than good for America’s top retirement program.

Image source: Getty Images.

The taxation of Social Security benefits is a necessary evil for America’s top retirement program

On paper, ending the taxation of benefits probably sounds great. Without this federal tax, somewhere in the neighborhood of half of all recipients would be able to hang onto more of the income they receive.

But this only tells one side of the story.

Since 1985, the annually released Social Security Board of Trustees Report has cautioned that America’s leading retirement program would contend with a long-term funding deficit. In other words, estimated revenue to be collected in the 75 years following the release of a Trustees Report would fall short of expected outlays (benefits paid to beneficiaries and, to a far lesser extent, administrative expenses to oversee the program), leading to a funding obligation shortfall.

As of the 2024 Trustees Report, this funding obligation shortfall stood at $23.2 trillion, and it’s been climbing with consistency for decades.

The silver lining for current and future retirees is that Social Security is in no danger of bankruptcy or insolvency. But this funding deficit does make clear that the existing payout schedule, including COLAs, isn’t sustainable. Based on estimates from the Trustees Report, the Old-Age and Survivors Insurance Trust Fund (OASI), which is responsible for doling out monthly checks to retired workers and survivor beneficiaries, is expected to deplete its asset reserves by 2033. Should this occur, sweeping benefit cuts of up to 21% may be needed to sustain payouts, without any further need for reductions, through 2098.

The Social Security program needs every cent in income it can get to avoid cutting benefits. Although the 12.4% payroll tax on earned income generates the lion’s share of income (about 91%) for Social Security, the taxation of benefits has been growing into an increasingly important source of income.

Over the next 10 years (2024 through 2033), the taxation of benefits is forecast to contribute a cumulative $943.9 billion to Social Security. If Trump were to remove this ancillary but growing source of income, Social Security would find itself in even worse financial shape, which may lead to the OASI’s asset reserves being depleted sooner than 2033.

Even though an overwhelming majority of Social Security beneficiaries despise the taxation of benefits, this necessary evil isn’t going anywhere.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.