benzinga.com

benzinga.com fool.com

fool.com

For most retirees, Social Security is a program they’d struggle to do without. An analysis from the Center on Budget and Policy Priorities estimated that Social Security pulled 22.7 million people out of poverty in 2022, roughly 16.5 million of whom were adults aged 65 and over.

Furthermore, 23 consecutive years of surveys from national pollster Gallup have shown that 80% to 90% of retirees lean on their payout in some capacity to cover their expenses. Social Security income is foundational to the financial well-being of most aging Americans.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

Unfortunately, the foundation of America’s leading retirement program isn’t so sturdy. Current and future retirees are counting on elected officials, including President-elect Donald Trump, to reform and strengthen Social Security — but fixing this program could prove more complicated than meets the eye.

President Trump overseeing a ceremony in the East Room of the White House. Image source: Official White House photo by Shealah Craighead, courtesy of the National Archives.

Social Security is potentially eight years away from sweeping benefit cuts

In January 1940, the first retired-worker benefit check was mailed. Every year since this milestone, the Social Security Board of Trustees has issued a report detailing the program’s financial health. In particular, the annual Trustees Report factors in changes to fiscal and monetary policy, as well as ongoing demographic shifts, to estimate the sustainability of Social Security payouts.

To be abundantly clear, the program is in no danger whatsoever of going bankrupt, becoming insolvent, or failing to pay eligible beneficiaries. However, continuing to pay benefits at existing levels, inclusive of cost-of-living adjustments (COLAs), is in question.

For 40 consecutive years, the Trustees Report has pointed to a long-term funding obligation shortfall. In simpler terms, the Trustees believe income collection in the 75 years following the release of a report will be insufficient to cover outlays, which includes benefits (inclusive of COLAs) and, to a lesser degree, the administrative expenses associated with running the Social Security program. As of 2024, this long-term cash shortfall tipped the scales at $23.2 trillion.

What’s far more worrisome is what might happen to the Old-Age and Survivors Insurance Trust Fund (OASI), which is responsible for paying benefits to retired workers and survivors of deceased workers.

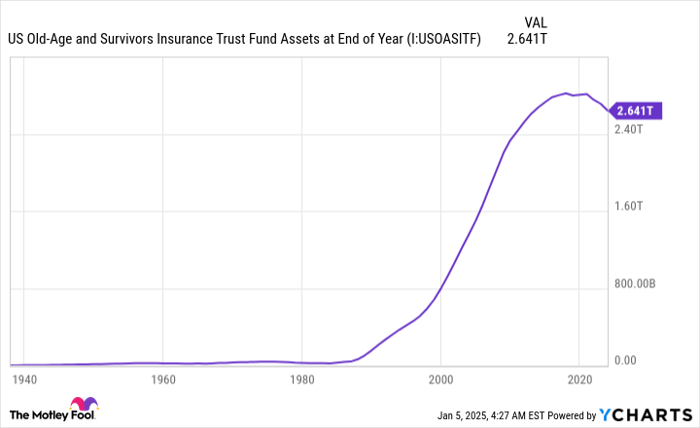

The Trustees Report predicts the OASI’s asset reserves — i.e., the excess cash built up since inception that’s invested in special-issue, interest-bearing government bonds — will be exhausted by 2033. If the OASI’s asset reserves disappear, a sweeping benefit cut of up to 21% may be needed to sustain payouts through 2098 without the need for any additional reductions.

While “congressional theft” and “undocumented migrants” are often incorrectly blamed for Social Security’s financial troubles, demographic changes, which include a historically low U.S. birth rate; rising income inequality; and a more than halving of net legal migration into U.S. since 1998, are primarily responsible for this mess.

The OASI’s asset reserves are forecast to be exhausted by 2033. US Old-Age and Survivors Insurance Trust Fund Assets at End of Year data by YCharts.

Incoming President Trump is facing a potential no-win scenario with Social Security

The all-important question is: How do lawmakers, including President-elect Trump, fix Social Security?

Although the incoming president has a few paths he could take, they could all result in America’s leading retirement program being worse off than he took office for a second time.

For example, in a December interview with Meet the Press, Trump was questioned about the possibility of reducing outlays for Social Security and Medicare. Trump responded by saying, “We’re not touching Social Security, other than we make it more efficient.”

This isn’t the first time Trump has proposed distancing himself and the Republican Party from attempting reforms on the nearly 90-year-old program. Said Trump, while speaking at the Conservative Political Action Conference in March 2013:

As Republicans, if you think you are going to change very substantially for the worse Medicare, Medicaid, and Social Security in any substantial way, and at the same time think you are going to win elections, it just really is not going to happen.

While doing nothing would likely avoid stirring the pot, kicking the can down the road for the next administration only makes Social Security’s problems worse. If the current projections from the Trustees prove accurate, the OASI would be four years away from benefit cuts when Donald Trump leaves office in January 2029.

Image source: Getty Images.

What’s popular isn’t always what’s best for Social Security

President-elect Trump might also choose to tackle Social Security reform head-on, as he intimated via social media post on Truth Social in late July. His post proclaimed, “Seniors should not pay tax on Social Security.“

In 1983, when Social Security’s asset reserves were running dangerously low, Congress passed and then-President Ronald Reagan signed the Social Security Amendments of 1983 into law. In addition to gradually increasing the payroll tax on earned income, as well as the full retirement age, it introduced the now-hated taxation of benefits.

Starting in 1984, up to 50% of benefits were subject to the federal tax rate if provisional income (adjusted gross income + tax-free interest + one-half of benefits) crested $25,000 for single filers or $32,000 for couples filing jointly. In 1993, the Clinton administration added a second tier that exposed up to 85% of benefits to federal taxation when provisional income topped $34,000 for single filers and $44,000 for couples filing jointly.

What really irks retirees is that these line-in-the-sand income thresholds have never been adjusted for inflation.

Though eliminating the taxation of benefits would increase Social Security checks for around half of all retirees, it would, by one analysis, cripple the program even further.

Between 2024 and 2033, taxation of benefits is expected to generate $943.9 billion in income for Social Security. Removing one of the program’s three sources of income would expedite the OASI’s asset reserve depletion date and potentially increase the amount benefits need to be cut to sustain payouts over the next 75 years, based on an analysis by the Committee for a Responsible Federal Budget.

But wait, there’s more

To make matters worse, amending the Social Security Act will require 60 votes in the upper house of Congress. The last time either party held a supermajority of votes (60) in the Senate was 1979. In short, changing Social Security will require bipartisan support, which has been hard to come by when it concerns America’s leading retirement program.

While Democrats and Republicans recognize that Social Security needs reform, they’ve approached these changes from opposite ends of the spectrum. Specifically, Democrats on Capitol Hill prefer increasing taxation on high earners, while Republicans predominantly want to increase the full retirement age and reduce long-term outlays.

Democrats in Washington, D.C., have been clear that they won’t vote in favor of changes that reduce Social Security outlays. Meanwhile, Republicans have been adamant that they won’t support legislation that targets high earners. This stalemate makes it highly unlikely that the Senate can get to the requisite 60 votes needed to enact meaningful Social Security reform.

Therefore, regardless of which Social Security strategy Donald Trump employs when he takes office in nine days, he may very well be facing a no-win scenario.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.