fool.com

fool.com retire.ly

retire.ly

For the more than 68 million people currently receiving a Social Security benefit, there’s no announcement more important than the cost-of-living adjustment (COLA) reveal during the second week of October.

Since 2002, national pollster Gallup has been conducting annual surveys to decipher how reliant retirees are on the income they receive from this top social program. Without fail, 80% to 90% of respondents, including 88% in April 2024, have stated that their Social Security check was a “major” or “minor” income source, and therefore necessary to make ends meet.

While Social Security’s 2025 COLA announcement offers superficial promise, the lack of a treasured silver lining will quickly take the luster off another above-average “raise” for beneficiaries.

Image source: Getty Images.

How is Social Security’s COLA calculated?

Social Security’s COLA is the tool the Social Security Administration (SSA) relies on to keep benefits from losing buying power over time. In other words, if the price for goods and services that retirees regularly buy increases, Social Security checks should rise by the same percentage to ensure no loss of purchasing power. Social Security’s “COLA” is the raise passed along most years that fights back against the effects of inflation.

In the 35 years following the mailing of the first Social Security check in January 1940, there was no rhyme or reason to when COLAs were passed along. After beneficiaries received no COLA in the entire 1940s, Congress approved the largest adjustment on record in 1950: an increase of 77%!

Beginning in 1975, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) became the inflationary tether used by the SSA to calculate annual price changes. The CPI-W contains more than 200 different spending categories, all of which have their own respective weightings. These weightings are what allow the CPI-W to be chiseled down to a single figure at the end of each month, making for simple year-over-year comparisons to see if prices have risen (inflation) or declined (deflation).

The interesting quirk about Social Security’s cost-of-living adjustment is that only the trailing-12-month readings ending in July, August, and September (the third quarter) are used in the calculation. If the average CPI-W reading for the third quarter of the current year is higher than the comparable period of the previous year, inflation has occurred, and a “raise” is on the way for beneficiaries.

The year-over-year percentage increase in average third-quarter CPI-W, rounded to the nearest tenth of a percent, represents the COLA for the upcoming year.

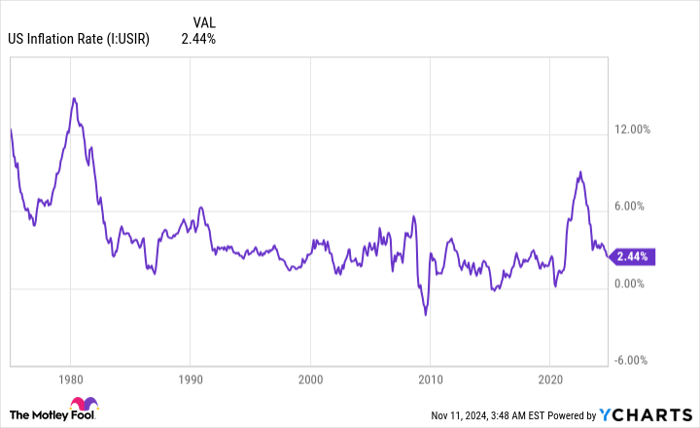

A big uptick in U.S. money supply sent the prevailing rate of inflation, as well as Social Security’s COLAs, soaring. US Inflation Rate data by YCharts.

An above-average cost-of-living adjustment is imminent

There’s been something of a night-and-day difference for Social Security recipients between the 2010s and 2020s. The 2010s featured the only three years of deflation over the last half-century, thereby resulting in no COLA being passed along in 2010, 2011, and 2016. Further, beneficiaries received the smallest positive cost-of-living adjustment in history (0.3%) in 2017.

But over the last four years, COLAs have meaningfully boosted Social Security checks — at least on a nominal-dollar basis. An unprecedented level of fiscal stimulus during the COVID-19 pandemic sent U.S. money supply soaring at the fastest rate in history, leading to a sizable uptick in the prevailing rate of inflation. The end result was a 5.9% COLA in 2022, an 8.7% raise in 2023, and a 3.2% increase in 2024. The payout boost in 2023 marked the highest on a percentage basis in 41 years.

Retirees who were hoping for an encore in 2024 weren’t disappointed. On Oct. 10, the SSA announced a 2.5% cost-of-living adjustment would be passed along to Social Security recipients come January 2025.

Even though a 2.5% increase to Social Security checks is the smallest in four years, it’s still modestly higher than the 2.3% average cost-of-living adjustment that’s been passed along since 2010.

According to estimates from the SSA, the average retired-worker beneficiary can expect their monthly payout to climb by $49 to $1,976 in the new year. More than 75% of the program’s 68.3 million beneficiaries are retired workers.

Meanwhile, the average monthly check for workers with disabilities and survivor beneficiaries is forecast to rise by $38 per month in 2025, respectively, to $1,580 and $1,551.

Image source: Getty Images.

A coveted Social Security silver lining has been ripped away once again

Unfortunately, not all is what it appears when it comes to Social Security’s cost-of-living adjustment.

In 2023, retired-worker beneficiaries were privy to a unique scenario. In addition to the largest COLA on a percentage basis since 1982, Medicare’s Part B premium declined by roughly 3.1% to $164.90/month from $170.10/month. Part B is the segment of Medicare responsible for outpatient services, and its premium is usually deducted from the Social Security checks of retirees aged 65 and above.

This decline in Part B in 2023 followed one of the largest year-over-year percentage increases in its history — 14.5% in 2022. This eye-popping increase had to do with the introduction of Aduhelm, an Alzheimer’s disease treatment from Biogen that has since been discontinued. Aduhelm carried a staggering annual cost of around $28,000 when 2022 began.

However, the Medicare program spent far less on Aduhelm than was initially anticipated, leading to a sizable uptick in the Supplementary Medical Insurance Trust Fund. The excess reserves collected in 2022 allowed for the premium offset of roughly 3% in 2023. Whereas Social Security’s COLA is meant to match the prevailing rate of inflation, this decline in the Part B premium actually allowed recipients to hang on to more of their monthly check.

Retired-worker beneficiaries aged 65 and older who are enrolled in traditional Medicare haven’t been as lucky over the last two years and have seen this silver lining ripped away.

Next-generation Alzheimer’s disease drugs are, once again, pushing Part B premiums notably higher. After a 5.9% increase to monthly premiums in 2024, the Centers for Medicare and Medicaid Services announced last week that the Part B premium will, again, climb by 5.9% — from $174.70 per month to $185.00 per month — in the upcoming year.

Although a 5.9% increase to the Part B premium is more palatable than the 14.5% hike passed along in 2022, it’s still more than double the 2.5% cost-of-living adjustment beneficiaries will receive come January. In other words, a potentially meaningful percentage of next year’s COLA will be offset by the rapidly rising Part B premium for most retirees.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

Sean Williams has no position in any of the stocks mentioned. The Motley Fool recommends Biogen. The Motley Fool has a disclosure policy.