fool.com

fool.com

For Social Security’s more than 68 million beneficiaries, nothing loomed larger last week than the annual reveal of the program’s cost-of-living adjustment (COLA).

Based on 23 years of annual surveys from Gallup, 80% to 90% of retirees (including 88% in 2024) have consistently pointed to their Social Security income as being necessary to make ends meet. For a majority of retired-worker beneficiaries, knowing how much they’ll be receiving each month in the upcoming year is critical information.

While Social Security’s 2025 COLA marks the fourth consecutive year of an above-average payout, it also comes with a sizable, and unavoidable, problem.

Image source: Getty Images.

What’s the purpose of Social Security’s COLA?

Every year, the price we pay for various goods and services fluctuates. Social Security’s famed COLA is the tool the Social Security Administration (SSA) has at its disposal to adjust benefits from one year to the next to account for these price changes.

For instance, if a good or service that retirees regularly buy increases in price by 5% from one year to the next, Social Security benefits would have to rise by a commensurate amount for retirees to still be able to afford this item, along with all of their other regular purchases. Social Security’s COLA is tasked with ensuring that beneficiaries don’t lose buying power over time.

Since 1975, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has been the inflationary tether for America’s top retirement program. The CPI-W has north of 200 different spending categories, each of which has their own respective weightings. These individual weightings are what allow the CPI-W to be expressed as a single figure on a trailing-12-month (TTM) basis, which makes for easy year-over-year comparisons to determine if collective prices are climbing (inflation) or falling (deflation).

Although the CPI-W is reported monthly by the U.S. Bureau of Labor Statistics, only the TTM readings ending in July, August, and September (the third quarter) factor into the cost-of-living adjustment calculation. If the average CPI-W reading in the third quarter of the current year is higher than the previous year, aggregate prices have risen, and beneficiaries are due for a “raise.”

This “raise,” (i.e., cost-of-living adjustment) is the year-over-year percentage difference in average third-quarter CPI-W readings, rounded to the nearest tenth of a percent.

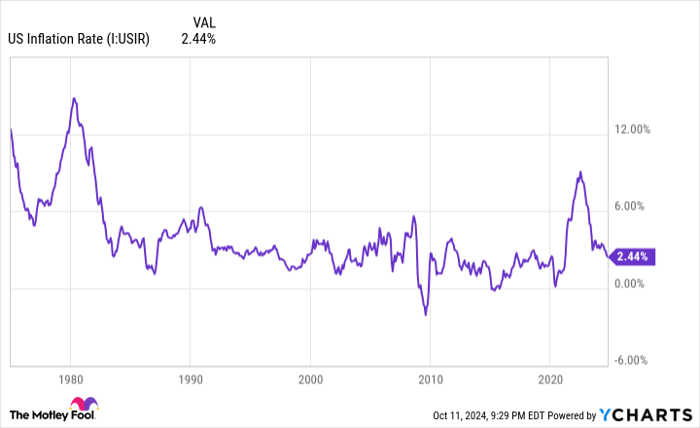

A sizable uptick in the prevailing rate of inflation has produced four above-average COLAs. US Inflation Rate data by YCharts.

A fourth consecutive above-average cost-of-living adjustment is on the way in 2025

Through the 2010s, Social Security COLAs were mostly forgettable. The decade featured three years when no COLA was passed along due to deflation (2010, 2011, and 2016), along with the lowest positive COLA in history — 0.3% in 2017. Thankfully, fortunes have changed for beneficiaries over the last couple of years.

In 2022, 2023, and 2024, the program’s COLA came in at 5.9%, 8.7%, and 3.2%, respectively. These markedly higher cost-of-living adjustments are a reflection of a meaningful increase in the prevailing rate of inflation, which was primarily driven by a historic expansion of U.S. money supply during the COVID-19 pandemic.

During spring and early summer, policy forecasters had suggested a real chance that Social Security’s 2025 COLA would make history. It’s been 32 years since the program’s COLA hit at last 2.7% in four consecutive years, and 28 years since COLAs reached 2.6% in four straight years. But following a deceleration of the prevailing rate of inflation in August and September, beneficiaries were forced to kiss history goodbye.

The good news is that Social Security’s 2025 cost-of-living adjustment is still above average for a fourth year in a row. Whereas the average COLA over the previous 15 years is just 2.3%, beneficiaries are set to receive a 2.5% boost to their monthly check come January.

Though this represents the lowest COLA in four years, the nominal-dollar increase in Social Security checks will be noticeable.

The average check for retired-worker beneficiaries, who make up 75% of all recipients and account for 81% of the benefits doled out monthly by the SSA, is set to climb by $49 per month to $1,976.

Meanwhile, the average monthly payout for workers with disabilities and survivor beneficiaries is expected to rise by $38 per month for both categories to $1,580 and $1,551, respectively.

Image source: Getty Images.

There’s a big problem with Social Security’s 2025 COLA

Although a fourth straight year with an above-average COLA is fantastic news on a nominal-dollar basis for Social Security’s aged beneficiaries, this “raise” is accompanied by a big problem: a persistent loss of purchasing power.

In a utopian world, the CPI-W would perfectly encompass the inflationary pressures that retirees are contending with, leading to accurate COLAs that ensure no loss of buying power. However, we don’t live in a utopian world, and the CPI-W is nowhere close to being a perfect inflationary measure for Social Security.

As its full name implies, the CPI-W tracks the spending habits of “urban wage earners and clerical workers.” These are typically working-age Americans who aren’t currently receiving a Social Security check. More importantly, they spend their money differently than the retirees who comprise the bulk of Social Security’s recipients.

Compared to working-age Americans, retirees spend a higher percentage of their monthly budget on shelter (the largest weighted component in the CPI-W) and medical care services. The CPI-W isn’t doing an adequate job of factoring in the magnitude of these inflationary pressures on seniors.

On a TTM basis, as of the end of September, the rate of inflation for shelter and medical care services was 4.9% and 3.6%, respectively, for the Consumer Price Index for All Urban Consumers (CPI-U), which is a similar inflationary measure to the CPI-W. As long as the rate of inflation for these two critically important expenses to retirees remains above the 2.5% COLA for 2025, it’s highly likely that beneficiaries will lose buying power next year.

To make matters worse, Medicare’s Part B premium is forecast to rise by 5.9% to $185 per month in 2025. Part B is the portion of Medicare that covers outpatient services, and this premium is usually deducted from the Social Security checks of retired workers aged 65 and over (the age of eligibility for traditional Medicare).

Next year marks the second consecutive year when the premium for Medicare Part B will climb by 5.9%. If this estimate proves accurate, it’ll minimize the impact of the coming 2.5% COLA for a majority of retirees.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.